$72 billion hiding in plain sight

The case for a Canadian GLP-1 programme — and a model for other countries

Marie, 54, in Montreal. Works in retail at $19/hour. Pre-diabetic and obese. No employer drug plan. Quebec’s public drug plan doesn’t cover GLP-1s for obesity. Cannot afford to self-pay for a GLP-1. Goes without.

James, 38, software engineer in Vancouver. Obese with hypertension. Employer drug plan covers his hypertension medication but excludes GLP-1s for obesity.

Priya, 42, stay-at-home mother in Brampton. Two kids, elderly father at home. No personal income; not in any employer plan. Ontario public drug coverage doesn’t cover GLP-1s for her obesity.

Three Canadians, three drug-coverage situations, same fiscal case. None with access today. All would have access under the proposed programme.

What if drugs could pay for themselves?

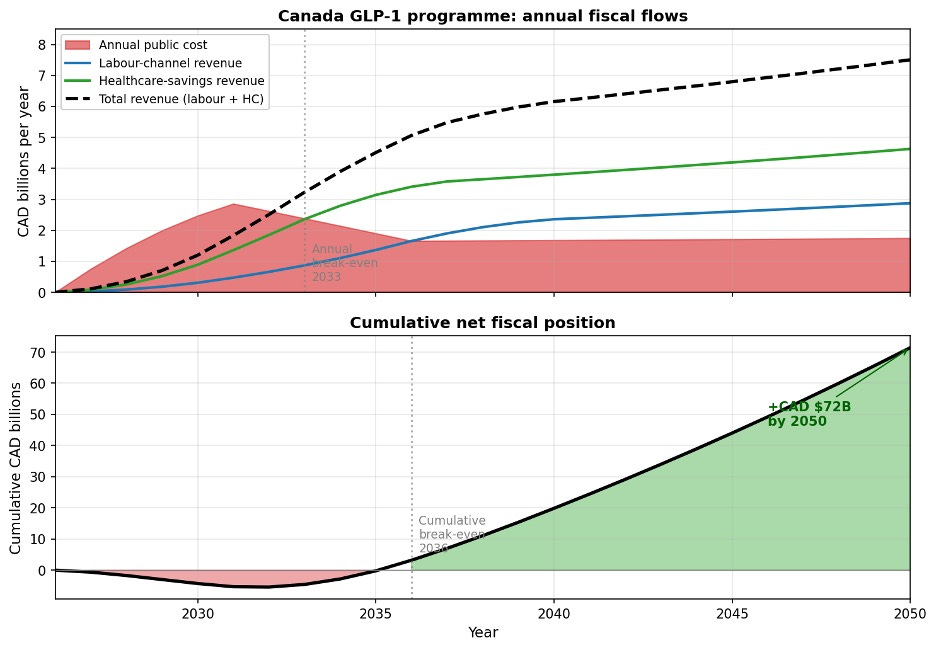

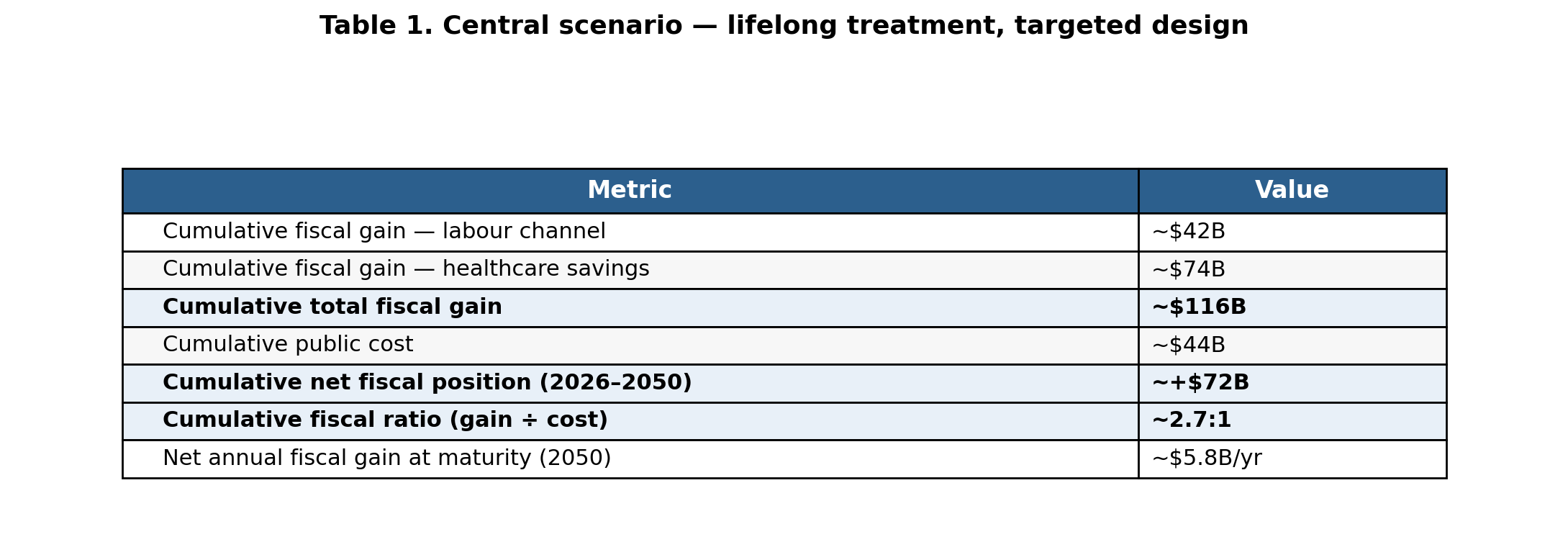

A well-designed Canadian GLP-1 programme would add approximately CAD $5.5 billion (0.14%) a year to GDP at maturity, turn fiscally positive in 2033, and produce a cumulative CAD $72 billion fiscal surplus by 2050. The fiscal ratio of approximately 2.7:1 outperforms average infrastructure, R&D subsidies, and most of what Canada currently spends on productivity and growth.

The worked example of Canada — and the programmatic choices — is informative for other countries. Canada is the first G7 country with generic access. Two generics have been approved with 7 more in regulatory review. The pan-Canadian Pharmaceutical Alliance framework prices generics at 35% of brand with three or more manufacturers — driving the expected stable-state price toward CAD $80 (US $59) per month, the figure used here.

I modelled the fiscal impact of GLP-1s in Canada, building upon earlier work by the Tony Blair Institute in the UK. The attached technical paper provides details. The argument here: GLP-1s for obesity belong in Canada’s public investment portfolio, where they hold zero place at present.

Two fiscal channels and the lifelong paradox.

The economic case flows through two distinct mechanisms.

The first is the labour market channel. When people with obesity lose weight and sustain that loss, they work more, work more productively, have lower disability rates. Tax revenues rise. Disability payments fall.

The second is the healthcare savings channel. Sustained weight loss prevents type 2 diabetes, cardiovascular events, musculoskeletal problems, and long-term care. These benefits phase in over three to ten years and keep growing as the cohort ages. Patients who stop semaglutide regain their lost weight. The healthcare savings channel requires lifelong treatment.

This is the lifelong paradox. A programme designed with a time cap — say, two years of coverage — is providing temporary weight reduction at public expense with no lasting fiscal benefit. In the model, a time-limited programme generates a cumulative fiscal deficit of approximately CAD $12 billion by 2050. A lifelong programme generates a surplus of approximately CAD $72 billion over the same period.

The figure and table below shows annual and cumulative fiscal flows.

Figure 1. Annual fiscal flows and cumulative net position, 2026–2050. Headline figures in Table 1 below.

Programme architecture: eligibility and two Canadian precedents.

On eligibility, I used the clinically warranted threshold of BMI ≥ 27 with one weight-related comorbidity — as used by clinical trials, and the US, Canadian, and European approved label. This eligible population is approximately 8.5 million Canadian adults aged 18 to 64. Any programme designed to the WHO BMI ≥ 30 obesity-only threshold systematically excludes much of the population the clinical evidence supports treating — including a large share of Asian-Canadian populations, where metabolic risk arrives at lower BMI.

The public coverage component follows the Canadian Dental Care Plan: income-tested at $90,000 household income, excluded if you have private drug insurance, co-payment structure sliding from zero to 25%, verified annually through tax filings. The Canadian dental plan covers 9 million Canadians at approximately $2.6 billion per year. A GLP-1 programme for the 2.3 million Canadians who lack any payer for the obesity indication and cannot self-pay would cost approximately $2.2 billion annually in drug costs at generic equilibrium pricing — comparable scale, proven administrative architecture. The means-test structure ensures the public programme does not displace private coverage; it targets the genuinely uncovered population only.

The employer component follows Quebec’s mandatory drug coverage model: applied here it would require employer drug plans that already cover obesity-related conditions — hypertension, type 2 diabetes, cardiovascular disease — to also cover Health Canada-approved GLP-1s for obesity, with no time cap. Approximately 4.7 million Canadians have employer plans that cover those conditions but explicitly exclude the obesity indication. The mandate corrects this at zero direct public cost.

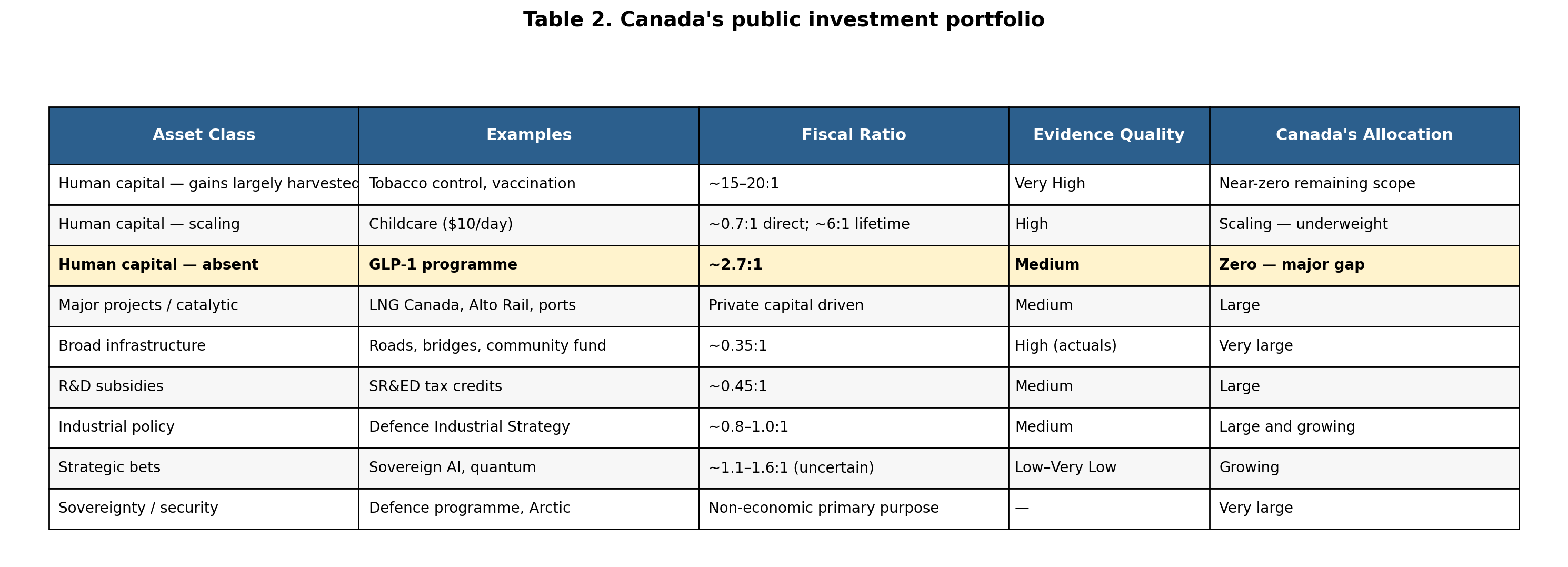

Portfolio: where GLP-1s sit in Canada’s public investment portfolio.

The most useful frame is not whether GLP-1s beat any individual competing programme. It is what kind of asset they represent, and whether Canada holds enough of that asset class.

Canada’s tobacco control programme returned approximately $20 for every public dollar invested between 2001 and 2016. Childhood vaccination returns approximately 18:1. The largest historical gains in Canada’s human-capital portfolio are programmes already at scale. The question is what comes next.

The childcare parallel is worth dwelling on. For most of the 1990s and 2000s, childcare was evaluated as social spending. The Quebec natural experiment changed that. Economists showed it raised maternal workforce participation, increased GDP, and generated fiscal returns exceeding programme cost over a long enough horizon. The evaluative frame shifted — from social spending to economic infrastructure — and the funding followed. GLP-1s need exactly the same move.

There is a fiscal-rule scoring problem behind this. A pharmacare programme costing $5 billion in year 1 scores as $5 billion in current-period deficit, even when it generates many times that in cumulative tax revenue and prevented healthcare costs over 25 years. The methodology that identifies this opportunity is not routinely applied. The methodology that is routinely applied does not identify it.

IMF Article IV consultations have repeatedly raised fiscal-rule modernization questions for Canada — including capital-investment treatment and multi-year horizon scoring. The Canada Growth Fund and Canada Infrastructure Bank already operate within multi-year horizons that current-period scoring does not capture; the recently announced Canada Strong Fund extends this approach further. GLP-1 programmes belong in the same fiscal-rule treatment. Cumulative-return scoring for human-capital investments is the institutional precondition for the rest of this argument to land.

GLP-1s at 2.7:1 outperform average infrastructure (0.35:1), R&D subsidies (0.45:1), and broad capital spending — with medium rather than low confidence, within a parliamentary term rather than a generation.

Canada’s public investment portfolio is long on venture capital and short on investment-grade bonds. GLP-1s are the most significant investment-grade human-capital opportunity currently available.

What this analysis can and cannot tell you

The CAD $72 billion figure is a central estimate from a country-specific model with a sensitivity range of approximately $30-120 billion across the parameters that carry meaningful uncertainty: real-world adherence at population scale, healthcare-savings ramp, real wage growth, and drug-price evolution.

Four structural features deserve flagging.

First, the healthcare-savings channel flows primarily to provincial budgets. The labour-channel tax capture flows primarily to federal coffers. The federal cabinet’s fiscal incentive is therefore weaker than the aggregate figure implies, absent cost-shared transfer architecture.

Second, the employer mandate is open to philosophic and Constitutional challenge. But the justification is straightforward: the benefit to cost ratio for employers is 5.1:1, greater than that for government. The fiscal case is also robust without a mandate. Voluntary coverage is rising as drug costs fall and employee pressure builds. Even without the mandate the fiscal surplus is almost cut in half but still positive. The mandate accelerates this trend and covers those — mostly in small business — who would not be covered. The mandate is a requirement that employers fund an investment returning many times its cost — one the collective action problem of the benefits market has prevented them from making individually. Implementation requires a federal-only mandate covering federally-regulated employers plus provincial coordination.

Third, the analysis lands in the middle of an unresolved Canadian pharmacare moment. Phase 1 of the Pharmacare Act covers contraception and diabetes medications through bilateral agreements with four jurisdictions; nine remain outside the program. The November 2025 federal budget allocated no new pharmacare funding. Current commitments expire in 2029. The GLP-1 case set out here is one worked example of a broader question — whether Canada analyzes pharmacare as current-period cost or as long-horizon fiscal investment. At the same time, it could focus the pharmacare debate on drugs that are fiscally positive investments.

Finally, the implementation of the childcare benefit is not flawless. One key difference between this programme and childcare is that the federal spending is means-tested. Nevertheless, this is an important reminder that the world is not about modelling but implementation.

These are not fatal constraints on the case. They are the architectural questions that matter for cabinet implementation, and they should be on the table when the policy is designed.

Canada as a model for other countries

What Canada does in the next 24 months matters beyond Canada. The next post shows that 19 of 21 high-income countries studied should launch their own programmes now at currently obtainable branded prices rather than waiting for patent expiration. Canada’s worked example — public coverage below an income threshold, employer mandate, lifelong design — is the closest available template for what those countries could be building. Canada launches first because it has generic access first. Canada sets the design. The global picture sets the scale — approximately $1.1 trillion across 55 modelled countries by 2050.

This is the second post in a series. The first reframed GLP-1s as longevity drugs and economic investments. This one is the worked example — Canada in detail — including how the programme should be designed and how it sits in the public investment portfolio. The third generalizes globally.

Disclosures: I own shares in Eli Lilly and Lir Life Sciences. I used AI (Claude from Anthropic) in economic modelling and to assist with research and drafting; the ideas and judgments are my own and I take full responsibility for them.

Thank you to Ilaria Calvello (Tony Blair Institute for Global Change) and Carsten Edwards for reviewing and commenting on earlier versions of the technical paper.

Here is the detailed technical paper:

This is a brilliant, highly compelling concept. I have some nagging concerns that long-term GLP-1 usage might have some negative side effects and impacts that we have not yet been able to see in the trials or general usage. If we would go whole-hog into mass usage ... and then see a mass negative impact to the population down the road ... that is a scary thought. But, I know the side effects seen thus far have been fairly minor, and these concerns may be unwarranted.

A thought-provoking piece on the enormous untapped potential of a national GLP-1 strategy in Canada — turning a public health challenge into a once-in-a-generation opportunity

Sharp analysis and bold vision systems-level thinking by @PeterASinger

.... as always

This is the kind of policy imagination healthcare desperately needs. 🇨🇦📊💊

#GLP1 #PublicHealth #HealthPolicy #ObesityCare #HealthcareInnovation